TL;DR

In Montgomery County, the 2026 conforming loan limit is $1,249,125 — one of the highest in the country. Because Bethesda’s median sale price is around $1.2M, many buyers can still finance with a conventional high-balance conforming loan at 5% down. Buyers purchasing above roughly $1.315M at 5% down will cross into jumbo territory, which requires a higher credit score (typically 700+), a 10–20% down payment, a DTI at or below 43%, and 6–12 months of cash reserves after closing.

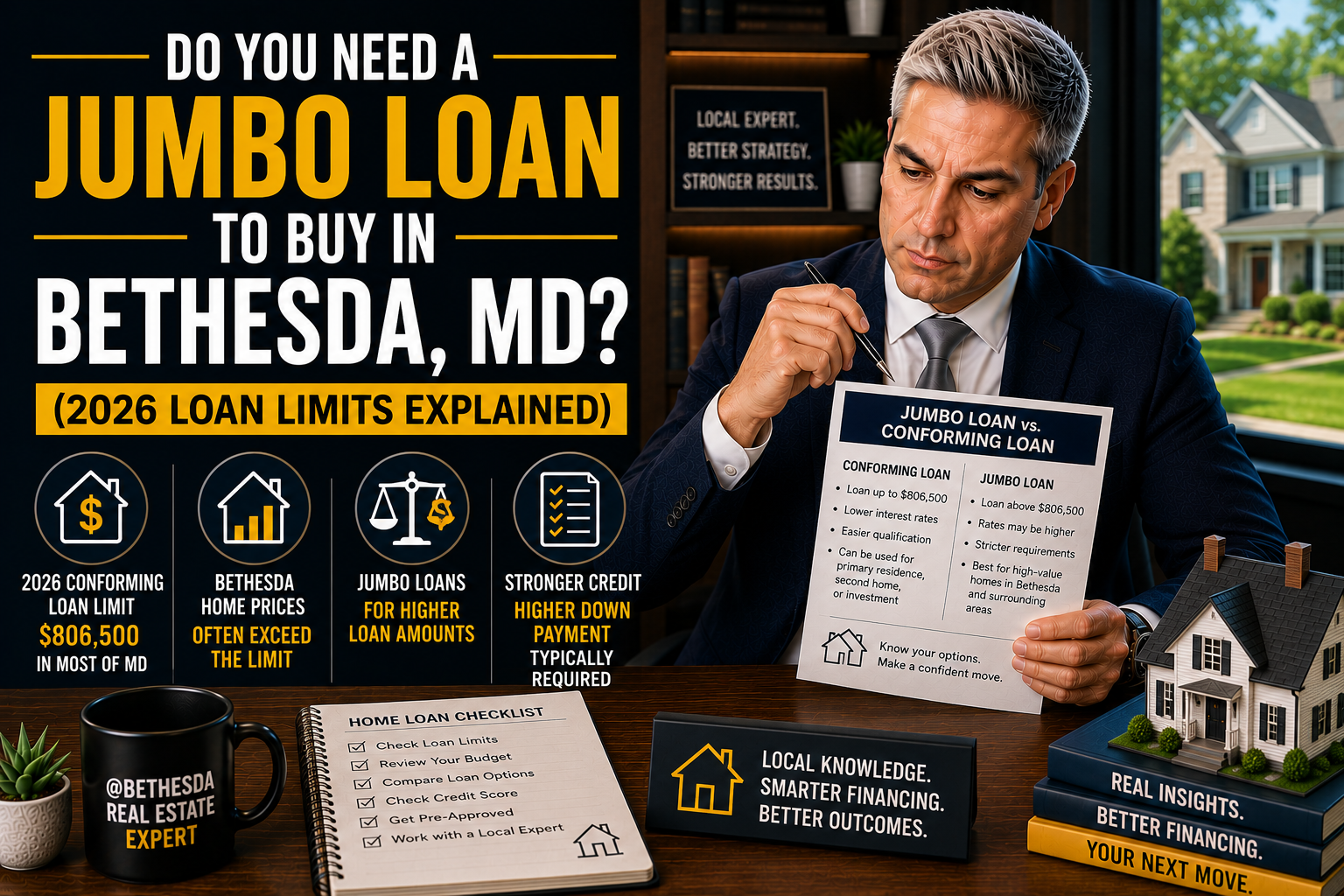

Do buyers in Bethesda, MD need a jumbo loan in 2026?

In Montgomery County, the 2026 conforming loan limit is $1,249,125 — one of the highest in the country. Because Bethesda’s median sale price is around $1.2M, many buyers can still finance with a conventional high-balance conforming loan at 5% down. Buyers purchasing above roughly $1.315M at 5% down will cross into jumbo territory, which requires a higher credit score (typically 700+), a 10–20% down payment, a DTI at or below 43%, and 6–12 months of cash reserves after closing.

By Pey Behin | May 15, 2026

When buyers first start looking in Bethesda, North Bethesda, or Potomac, one of the first questions they ask is whether they’ll need a jumbo loan. It’s a fair question — homes here regularly trade between $1M and $2M, and “jumbo” sounds like a word that applies to all of them.

The reality is more nuanced. Whether or not you need a jumbo loan matters a lot — it affects your down payment, your debt-to-income ceiling, the credit score you need, and the cash reserves your lender will require after closing.

Here’s how it actually works in Montgomery County in 2026, and how to figure out which side of the line you’re on before you start making offers.

The Conforming Loan Limit for Montgomery County

Every year, the Federal Housing Finance Agency sets a conforming loan limit — the maximum mortgage amount that Fannie Mae and Freddie Mac will purchase. Because Montgomery County is part of the Washington, DC metro area, it qualifies as a “high-cost” area, which means it gets a significantly higher limit than most of the country.

For 2026, the conforming limit for a single-unit property in Montgomery County is $1,249,125.

Any loan at or below this amount qualifies as conforming — sometimes called a “high-balance conforming” loan in this price range, but still underwritten to conventional standards. Any loan above $1,249,125 is a jumbo loan, and different — more demanding — qualification rules apply.

This limit applies across the DC metro tier, which includes Montgomery County, Prince George’s County, DC, Arlington, and Fairfax. If you’re buying in Bethesda, Chevy Chase, Potomac, or North Bethesda, you’re in a high-cost area and that $1.249M ceiling is yours to work with.

What This Means for Buyers in Bethesda

Bethesda’s median sale price is around $1.2M as of early 2026 — and with the high-cost conforming limit at $1,249,125, a lot of buyers in this market can stay in conforming range depending on their purchase price and down payment.

Here’s the math most buyers don’t run until too late:

- 5% down on a $1.2M home: Loan = $1,140,000 → conforming

- 5% down on a $1.32M home: Loan = $1,254,000 → jumbo

- At 5% down, the conforming ceiling is roughly $1.315M in purchase price

Put differently: in Montgomery County, you can buy up to about $1.315M with a 5% down conforming loan. Above that, you’re in jumbo territory.

For first-time buyers, 3% down conforming options exist under the high-balance tier, theoretically extending conforming reach to roughly $1.287M in purchase price. Not all first-time buyer programs support high-balance loans, so that’s worth confirming with your lender before you assume.

Homes in upper Bethesda and Potomac — $1.5M, $1.8M, $2M+ — will almost always require jumbo financing regardless of down payment, simply because the loan amount itself exceeds the limit.

What Changes When You Go Jumbo

Going jumbo doesn’t disqualify you — plenty of buyers in Bethesda use jumbo financing every month. But it changes the rules in ways that can catch people off guard if they haven’t prepared.

Down payment. Conforming loans allow 3–5% down. Jumbo loans typically require 10–20%. If you’ve budgeted 5% down on a home that ends up needing jumbo financing, you need to recalculate.

Debt-to-income ratio. Conforming loans can accommodate DTIs up to 50%. Jumbo loans typically cap at 43% — and some lenders hold stricter limits. If you carry a car loan, student debt, or other obligations, this cap can push you out of the market at a price point you thought you could reach.

Credit score. Conforming loans are accessible with scores as low as 620. Jumbo lenders typically require 700 or higher, and most want 720+. A buyer who qualifies easily for conforming may hit friction at the jumbo threshold.

Cash reserves. This is the one that surprises people most. Jumbo loans almost always require 6–12 months of mortgage payments saved in liquid assets after closing. On a $1.5M purchase with 10% down, that might mean an additional $60,000–$80,000 in verifiable post-close reserves — on top of your down payment and closing costs. If you’re tapping most of your liquid assets to close, this requirement becomes a real constraint.

Closing timeline. Jumbo loans often require an additional appraisal review step, which can add 7–10 days to underwriting. This matters when you’re negotiating settlement dates and inspection contingency windows in a competitive offer.

When Going Jumbo Can Work in Your Favor

There are situations where jumbo financing at a larger down payment is actually competitive with — or better than — conforming.

With 15–20% down, some jumbo loan products eliminate private mortgage insurance and price their rates very close to conforming. For buyers in the $1.4M–$2M+ range who have the equity to put 15–20% down, your lender should model both options: conforming with PMI versus jumbo without PMI. The monthly cost difference can be more favorable on the jumbo side than you’d expect.

Jumbo loans also tend to be less sensitive to the loan-level price adjustments that can increase conforming loan rates for borrowers with certain down payment percentages or credit profiles. If your situation involves a lower down payment and a credit score in the 680–720 range, your lender may find that a jumbo product actually prices better for you.

What to Know Before You Start Looking

The jumbo question isn’t just a financing issue — it affects your offer strategy. A buyer with jumbo financing needs a lender who can credibly underwrite that product and close on time. Not every lender who handles conforming loans is equally experienced with jumbo deals, and the difference shows up in closing delays and stalled underwriting.

Before your first showing, you need to know:

- The exact conforming/jumbo threshold for your target purchase price and down payment

- Your DTI with a mortgage at your target price — and whether it clears the jumbo cap

- Your post-closing reserves, not just your down payment and closing costs

- Whether any of your funds are gifts, and how that interacts with jumbo underwriting

- How long your lender’s jumbo process typically takes, so you negotiate contingency periods accordingly

If you’re thinking about asking for a seller concession to offset closing costs on a jumbo loan, your lender needs to know that upfront — jumbo guidelines on seller-paid closing costs may differ from conforming limits. And if you’re using equity from a current home as part of your down payment, the bridge loan vs. sale contingency picture changes depending on whether you land in conforming or jumbo range on the new purchase.

Your first conversation should be with a lender who knows this market — not an algorithm.

Frequently Asked Questions

What is the conforming loan limit for Montgomery County, MD in 2026?

The 2026 conforming (high-balance) loan limit for Montgomery County is $1,249,125 on a single-unit property. Montgomery County is part of the DC metropolitan statistical area, which qualifies as a high-cost area under FHFA guidelines. The standard national baseline is $832,750 — the higher limit applies specifically because of the DC metro high-cost designation.

At what purchase price do Bethesda buyers need a jumbo loan?

With 5% down, buyers cross into jumbo territory at purchase prices above roughly $1.315M, since that’s where the loan amount exceeds $1,249,125. With 10% down, the threshold rises to about $1.388M. With 20% down, you can reach approximately $1.561M before needing jumbo financing. Your exact threshold depends on your down payment percentage, so confirm with your lender for your specific situation.

What credit score do you need for a jumbo loan in Maryland?

Most jumbo lenders in Maryland and the DC metro area require a minimum credit score of 700, with many preferring 720 or higher. This is a meaningful step up from conforming loans, which are available with scores as low as 620. If your score is in the 680–720 range, a lender may still find a jumbo product, but terms will be less favorable.

Can you get a jumbo loan with 10% down in Maryland?

Yes, 10% down is available on many jumbo products in Maryland. You’ll typically still need to meet the stricter DTI cap (around 43%) and the post-closing reserve requirement — 6–12 months of mortgage payments in liquid assets after your down payment and closing costs are paid. At 10% down, some lenders will require PMI; others structure jumbo products to avoid it.

Is a jumbo loan more expensive than a conventional loan in 2026?

Not necessarily. Jumbo loan rates in 2026 are competitive with conforming rates and sometimes lower for borrowers with strong credit and larger down payments, where jumbo products avoid the loan-level price adjustments that can increase conforming pricing. The bigger cost factor with jumbo loans isn’t the rate — it’s the larger down payment and the post-closing reserve requirement, which together mean you need more liquid capital to close.

Buying in Bethesda or Potomac in the $1.2M–$2M range means spending time upfront on your financing structure before you start competing for homes. Whether you end up in conforming or jumbo territory isn’t something to discover at the pre-approval stage — it should be mapped out before you set a target price.

If you want to run through where you’d land and what it means for your offer strategy, reach out. It’s a twenty-minute conversation that changes everything about how you search.

About Pey Behin

Pey Behin is a residential real estate agent serving the Washington, DC metro area, with a focus on Bethesda, Montgomery County, and Northern Virginia. He works with buyers and sellers who want clear strategy, data-driven pricing, and direct guidance throughout the transaction process. His approach combines market analytics, negotiation expertise, and modern marketing to position clients effectively in competitive conditions.

Talk to Pey Directly

Questions about the Bethesda or DC Metro market? I respond fast.

Let's Connect