TL;DR

Move-up buyers in Bethesda have two real options: a bridge loan (borrow against your current home’s equity at 8–11% APR, with total costs typically running $12,000–$22,000 for a six-month loan) or a sale contingency (your offer depends on selling first, but it weakens your position in a multiple-offer market). In Montgomery County, where homes sell in roughly 34 days and clean offers routinely win, most buyers with strong equity lean toward a bridge loan or a coordinated same-day close. The right path depends on your equity, debt-to-income ratio, and how quickly your home will move.

How can you buy a home before selling yours in Bethesda, MD?

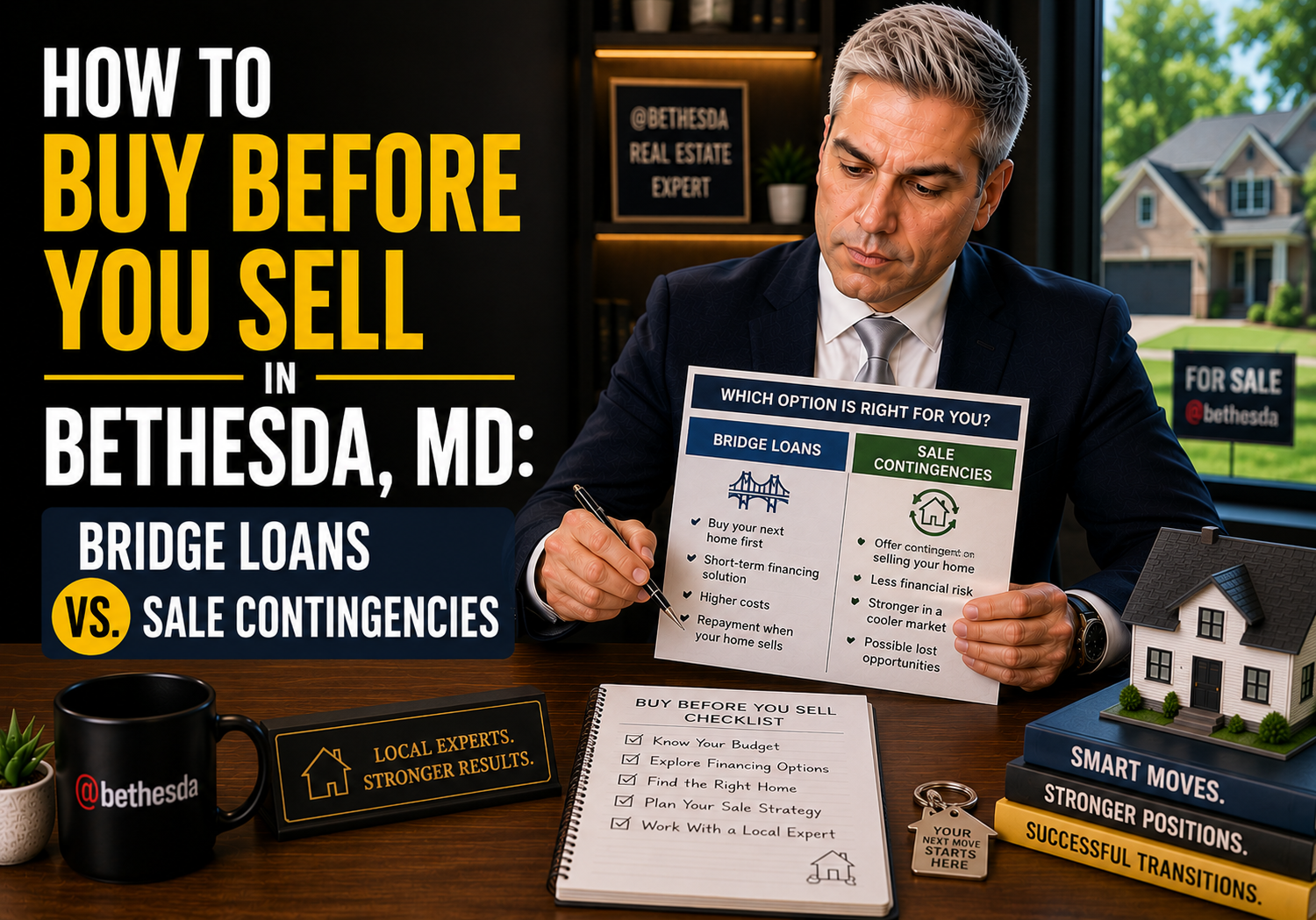

Bethesda move-up buyers have two main paths: a bridge loan — a short-term loan against your current home’s equity at 8–11% APR — or a sale contingency, which makes your purchase conditional on selling first. Bridge loans let you make a competitive, non-contingent offer but carry real costs (typically $12,000–$22,000 for a six-month bridge). Sale contingencies protect your downside but frequently lose to cleaner offers in the competitive Bethesda and Montgomery County market, where the median sale price is around $1.2M and multiple-offer situations remain common.

By Pey Behin | May 7, 2026

If you own a home in Bethesda and you’re ready to move up, the timing math can feel impossible.

You need the equity from your current home to fund your next purchase. But you can’t access that equity until you sell. And in a market where the right house in North Bethesda or Potomac might go under contract in a week, waiting until you’ve closed before you start seriously shopping feels like a losing strategy.

This is the move-up buyer’s dilemma. It comes up constantly among homeowners in the $700,000–$2,000,000 range. There are two real solutions: a bridge loan or a sale contingency. Both work. Neither is perfect. Which one makes sense depends on your specific situation.

If you’ve been thinking through whether to sell first before buying, this is the other side of that conversation — what your options actually look like if you want to buy before you sell.

Option 1: The Bridge Loan

A bridge loan is a short-term loan secured against the equity in your current home. It bridges the financial gap between your next purchase and the sale proceeds you’re waiting on.

How it works:

- You apply for a bridge loan using your current home as collateral

- The lender advances you funds — typically 70–80% of your available equity after your existing mortgage balance

- You use those funds to close on your new home, often without a sale contingency in your offer

- You list and sell your current home on a normal timeline

- Sale proceeds pay off the bridge loan in full

What it costs in 2026:

Bridge loan interest rates in the DC metro area currently run 8–11% APR, depending on the lender, loan size, and your financial profile. Most bridge loans don’t require monthly payments — interest accrues and is repaid when your home sells.

On a $350,000 bridge carried for six months, expect total costs between $15,000 and $22,000, including origination fees and interest. On a $250,000 bridge, you’re looking at $12,000–$16,000. That’s real money. But if a clean offer helps you win a home at the right price — or lets you negotiate from a position of strength — the math can work in your favor.

The main advantage:

You can make a non-contingent offer. In Bethesda, where the median sale price is around $1.2 million and multiple offers are common, this is significant. Sellers don’t want to take their home off the market for a buyer whose purchase depends on selling their own property first. A bridge loan removes that dependency and lets you compete on the same terms as any unencumbered buyer.

The risks:

If your current home takes longer to sell than expected, you carry two properties. If it sells for less than your CMA projected, net proceeds might not fully cover the bridge payoff. Before committing, run both the expected scenario and a conservative one with your lender. Knowing your projected net from the sale — not a Zillow estimate, but an actual number — is where this analysis has to start.

Not every lender offers bridge products, and your debt-to-income ratio with a bridge loan on top of your existing mortgage needs to clear underwriting. Engage your lender early.

Option 2: The Sale Contingency

A sale contingency is a clause in your purchase offer making it conditional on the successful sale of your existing home.

You make an offer on the new property, but the contract includes language stating that the purchase depends on your current home selling by a defined date. If your home doesn’t sell in time, you can exit the contract without forfeiting your earnest money deposit.

The challenge in a competitive market:

Most sellers in the Bethesda area don’t welcome sale contingencies. You’re asking them to take their home off the market — or accept more uncertainty — while you execute your own sale. In a multiple-offer situation, this typically costs you the deal. Sellers choose the cleanest offer available when they have options.

Many sellers who do accept a contingent offer will counter with a kick-out clause — a provision allowing them to continue marketing and, if a better offer arrives, giving you a defined window (typically 48–72 hours in Maryland) to remove the contingency or walk away. It’s worth understanding how contingencies work in Maryland contracts before you include one.

When a sale contingency makes sense:

If you have a highly marketable home you expect to sell quickly, and you’re buying a property that isn’t attracting multiple offers, a sale contingency can work. It protects your downside — you won’t end up owning two homes. In a softer pocket of the market, or with a seller who needs flexibility more than speed, this is a reasonable path.

In a typical Bethesda multiple-offer situation on a well-priced home, though, a sale contingency often costs you the deal entirely.

Option 3: The Coordinated Same-Day Close

Some move-up buyers avoid bridge loan costs and the contingency problem by coordinating a simultaneous close — selling their current home and purchasing the next one on the same day, with proceeds flowing directly from one transaction to the other.

This requires careful coordination between your agent, lender, and both settlement companies. Your sale closes first; proceeds wire immediately into the purchase settlement. When it works, it’s elegant and cost-free.

The challenge: if anything on the sell side runs into a last-minute delay — a buyer’s financing issue, a title problem, a late wire — your purchase settlement is at risk. A coordinated same-day close leaves almost no margin for the unexpected. In a clean, straightforward sale, it’s a real option. In anything more complicated, it’s a high-wire act.

How to Decide

Before choosing a path, you need actual numbers — not rough estimates.

- Your home’s realistic sale price based on a current market analysis

- Your equity after your mortgage payoff

- Your debt-to-income ratio with a bridge loan added to your existing mortgage

- Your home’s estimated days-on-market based on recent comps and current inventory

A bridge loan is worth its cost if your equity is strong, your home will move quickly, and you’re buying in a competitive situation. A sale contingency is a better fit if you need more runway on the sell side, your equity is more moderate, or you’re targeting a property with less competition.

Get your lender involved before you start searching. They determine whether a bridge loan is even on the table, and they can model the bridge scenario alongside your existing mortgage in a single conversation. Every move-up buyer situation I’ve worked with goes better when the lender is in the room from the beginning — not after you’ve already fallen for a property.

Your equity position, your home’s marketability, and your risk tolerance determine the right call. That’s exactly the kind of analysis I walk every move-up buyer through before we start searching. If you want to run the numbers before you’re under time pressure, reach out — it’s a short conversation that makes the whole process cleaner.

Frequently Asked Questions

How much equity do I need to qualify for a bridge loan in Maryland?

Most Maryland lenders require at least 20–30% equity after accounting for your existing mortgage balance. You can typically borrow 70–80% of your net equity. On a Bethesda home worth $1.1M with a $500K mortgage balance, your accessible equity might support a bridge loan of $300,000–$400,000. Your lender will calculate the exact figure based on a current appraisal and your full financial profile.

Will a sale contingency automatically disqualify my offer in Bethesda?

Not automatically — but in a competitive situation it significantly weakens your position. In a multiple-offer situation on a well-priced home in Bethesda, Potomac, or North Bethesda, sellers almost always choose a cleaner offer when one is available. A sale contingency is more viable when you’re the only bidder, when the property has been sitting on the market, or when you can offset the contingency with a larger earnest money deposit or a flexible settlement date.

What is a kick-out clause and how does it work in Maryland?

A kick-out clause lets the seller continue marketing after accepting a contingent offer. If a better offer comes in, the seller notifies you and you typically have 48–72 hours to remove your contingency and proceed — or walk away. Maryland contracts frequently include kick-out provisions when sellers accept sale contingencies in an active market, so it’s important to understand that a contingent accepted offer is not the same as a firm accepted offer.

What are the alternatives to a bridge loan if I want to buy before selling?

A home equity line of credit (HELOC) can serve a similar function at a lower interest rate, but typically takes 2–4 weeks to set up and isn’t available on all properties. Some buyers use retirement accounts or gift funds to cover the gap. A coordinated same-day close — where your sale and purchase both settle on the same day — eliminates bridge financing costs but requires everything on the sell side to go smoothly with no margin for delay.

What if I can’t qualify for a bridge loan because of my debt-to-income ratio?

This is common for buyers who already carry a significant mortgage. In that case, a sale contingency with a kick-out clause may be your only financed path. Some buyers in this situation choose to sell first and rent short-term while they search — it’s not glamorous, but it’s a clean path that makes you a fully competitive buyer with no contingencies when you do make offers.

Move-up buyers in Bethesda and Montgomery County face real timing constraints that don’t have one universal answer. The right path — bridge loan, sale contingency, or coordinated close — depends on your specific numbers and how your home is likely to move.

If you want to work through which option fits your situation before you’re under pressure, I’m happy to do that. Reach out anytime.

About Pey Behin

Pey Behin is a residential real estate agent serving the Washington, DC metro area, with a focus on Bethesda, Montgomery County, and Northern Virginia. He works with buyers and sellers who want clear strategy, data-driven pricing, and direct guidance throughout the transaction process. His approach combines market analytics, negotiation expertise, and modern marketing to position clients effectively in competitive conditions.

Talk to Pey Directly

Questions about the Bethesda or DC Metro market? I respond fast.

Let's Connect