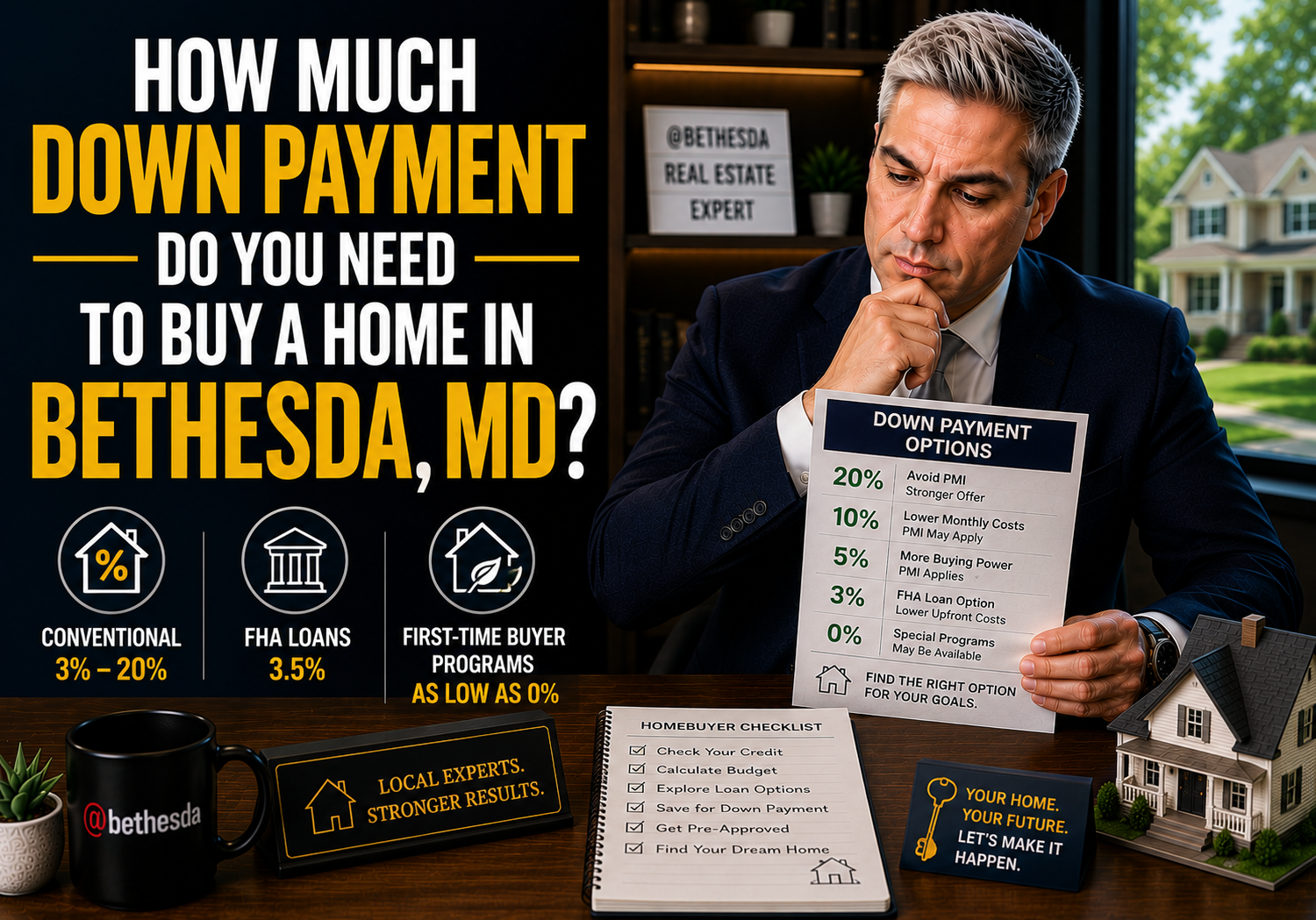

How much down payment do you need to buy a home in Bethesda, MD?

In Bethesda and Montgomery County, buyers can qualify for conventional loans up to $1,209,750 with as little as 3–5% down. FHA loans go up to $1,249,125 with 3.5% down. For homes priced above those thresholds — common in Bethesda — jumbo financing typically requires 10–20% down. The 20% figure that most buyers hear is not a requirement; it’s the threshold where private mortgage insurance (PMI) drops off.

By Pey Behin | May 2026

Most buyers walk into Bethesda thinking they need 20% down. On a $1.2M home, that’s $240,000 sitting in cash before you even look at closing costs. So they either delay the search, deplete their savings, or assume the market isn’t for them yet.

That math is wrong — or at least, it’s incomplete.

Montgomery County is a federally designated high-cost area, which means the loan limits that apply here are significantly higher than the national baseline. A buyer with good credit and a stable income has more options than they realize. Here’s how the numbers actually break down.

The Conventional Loan: 3–5% Down Up to $1.2M

The most common loan type for Bethesda buyers is a conventional mortgage — either through Fannie Mae or Freddie Mac. In 2026, the conforming loan limit for Montgomery County is $1,209,750. That’s the high-cost area ceiling, not the national floor.

What that means: you can finance up to $1,209,750 with a conventional loan. For a $1.2M home with 5% down, your loan amount is $1,140,000 — still under the cap. You qualify for standard Fannie/Freddie pricing.

Minimum down payments on conventional loans:

- 3% down — available to first-time buyers through certain programs (Fannie’s HomeReady, Freddie’s Home Possible)

- 5% down — the standard minimum for most conventional borrowers

- 10% down — often required for second homes or certain condo types

You’ll pay private mortgage insurance (PMI) if your down payment is under 20%. On a conventional loan, PMI is not permanent — it drops off once you reach 20% equity, either through payments, appreciation, or a combination. Rates vary, but budget roughly 0.5–1.0% of the loan amount annually until you hit that threshold.

At a $1M purchase price with 5% down, you’re financing $950,000. PMI at 0.7% adds roughly $554/month until you’ve built enough equity. That’s real money, but it’s not a reason to delay buying if the market and your finances align.

The FHA Loan: 3.5% Down, High Limits in Montgomery County

FHA loans have a reputation for being the “lower credit” option, but in Montgomery County they’re a legitimate choice even for well-qualified buyers — because the FHA loan limit here is $1,249,125.

That means you can buy a home up to $1.25M with just 3.5% down (assuming a 580+ credit score). On a $1.2M home, that’s $42,000 down. On a $900K home, it’s $31,500.

What FHA gives you: a lower credit score floor (580 vs. 620+ for conventional), more flexibility on debt-to-income ratios, and the ability to use gift funds for the entire down payment.

The tradeoff: FHA loans carry mortgage insurance premium (MIP), which is 1.75% upfront (usually financed into the loan) plus 0.55% annually for the life of the loan if you put less than 10% down. Unlike conventional PMI, FHA’s annual premium doesn’t automatically drop when you hit 20% equity — you’d need to refinance to remove it.

For buyers with credit scores in the 580–680 range, or who are stretching their savings thin to make the purchase work, FHA can be the right call. For buyers with strong credit who plan to stay long-term, the lifetime MIP is worth modeling out versus a conventional loan with PMI that will eventually fall off.

Above $1.25M: Jumbo Territory

Bethesda’s median sale price runs $1.1M–$1.5M depending on the neighborhood and property type. A meaningful share of homes — especially in Chevy Chase, Potomac, and North Bethesda — trade above the conforming and FHA limits.

Once you’re above $1,209,750 (conventional) or $1,249,125 (FHA), you’re in jumbo loan territory. Jumbo loans are not backed by Fannie, Freddie, or FHA — they’re portfolio products held by individual lenders, which means the requirements are set by each lender.

General guidelines for jumbo loans in 2026:

- Minimum down payment: typically 10–20%, though some lenders offer 10% jumbo products for well-qualified borrowers

- Credit score: usually 700+, often 720+ for the best pricing

- Reserves: most jumbo lenders want to see 6–12 months of mortgage payments in liquid assets after closing

- Debt-to-income: typically capped at 43%, stricter than FHA

On a $1.5M home with 10% down, your loan is $1,350,000. That’s a jumbo. Rates on jumbo products in 2026 are competitive — sometimes at or below conventional rates for highly qualified buyers — but the approval process is more demanding.

If you’re buying in this range, your lender selection matters more than at lower price points. Not all lenders offer competitive jumbo products, and the difference in rate can be significant.

The 20% Question

You don’t need 20% down to buy in Bethesda. But there are real advantages to getting there if you can.

At 20% down: no PMI, lower monthly payment, lower loan-to-value ratio (which often means better rate pricing), and stronger negotiating position in competitive situations where sellers weigh financing strength.

At 10–15% down: you’re in conventional or jumbo territory with PMI, slightly higher rates, but meaningfully less cash out the door at closing.

At 3–5% down: viable on homes under $1.2M, with PMI factored in. Leaves more liquidity for reserves, repairs, and normal life after closing.

The right number depends on your cash position, your timeline, and how you weigh monthly payment against preserved savings. Every situation is different, and the only way to know what makes sense for yours is to run the actual numbers — not the rule of thumb.

I walk buyers through this exact analysis before they start touring homes. Understanding your real purchasing power changes how you approach the market.

Down Payment Assistance in Montgomery County

If you’re a first-time buyer — meaning you haven’t owned a home in the past three years — Montgomery County has a program worth knowing about.

The Montgomery Homeownership Program (MHP), run through the Maryland Mortgage Program, provides a deferred second mortgage of up to $50,000 for down payment and closing costs. Zero percent interest. Repayment is deferred until you sell, refinance, or transfer the property.

Income limits apply ($196,680 for 1–2 person households, $229,460 for 3+), and you must purchase through an MMP-approved lender. But for buyers who qualify, this can cover a significant portion of what would otherwise come out of pocket.

Understanding your buyer closing costs in Bethesda alongside your down payment requirements gives you a complete picture of what you need to bring to the table. And if you haven’t already lined up representation, reviewing a buyer broker agreement is a smart early step in Maryland.

Frequently Asked Questions

Can I really buy a $1M home in Bethesda with less than 20% down?

Yes. On a home priced at or below $1,209,750, conventional financing allows as little as 5% down with PMI. FHA loans permit 3.5% down up to $1,249,125 in Montgomery County. The 20% figure avoids mortgage insurance but is not a requirement for financing.

What’s the minimum credit score to buy in Bethesda?

For FHA loans, 580 qualifies for 3.5% down. Conventional loans typically require 620+, though better pricing starts at 700+. Jumbo loans (above $1.2M) usually require 700–720 minimum. Your rate is heavily influenced by your score tier.

Does the down payment amount affect my offer competitiveness?

In Bethesda’s competitive market, sellers do consider financing strength. A 20% down offer is perceived as lower risk than 3.5% down, particularly in multiple-offer situations. That said, a well-structured offer with strong pre-approval can compete effectively at lower down payment levels. Your agent’s guidance on how to position the offer matters as much as the number itself.

What’s a jumbo loan and when do I need one in Bethesda?

A jumbo loan is any mortgage above the conforming limit — in Montgomery County, that’s $1,209,750 for 2026. Homes priced above roughly $1.27M (assuming 5% down) will require jumbo financing. Minimum down payments typically start at 10%.

Can I use gift funds for my down payment in Bethesda?

Yes. FHA loans allow 100% of the down payment to come from gift funds. Conventional loans allow gifts for down payments of 20% or more, and allow partial gifts at lower down payment levels depending on the loan program. Your lender will specify documentation requirements.

The down payment question doesn’t have one answer — it has five or six, depending on your loan type, the purchase price, your credit, and what programs you qualify for. Getting pre-approved with a lender who knows Montgomery County’s specific limits is the fastest way to know exactly where you stand.

If you want to talk through your situation before you start looking, I’m happy to help you run the numbers. Reach out anytime.

About Pey Behin

Pey Behin is a residential real estate agent serving the Washington, DC metro area, with a focus on Bethesda, Montgomery County, and Northern Virginia. He works with buyers and sellers who want clear strategy, data-driven pricing, and direct guidance throughout the transaction process. His approach combines market analytics, negotiation expertise, and modern marketing to position clients effectively in competitive conditions.

Talk to Pey Directly

Questions about the Bethesda or DC Metro market? I respond fast.

Let's Connect