One mortgage point costs 1% of the loan amount and typically reduces your rate by 0.25%. On a $1M Bethesda jumbo loan, one point = $10,000 upfront to save ~$165/month. The break-even is about 60 months. Points make sense if you're staying 5+ years and rates don't drop enough to refinance first.

Should You Pay Mortgage Points to Lower Your Rate? A Bethesda Buyer's Guide

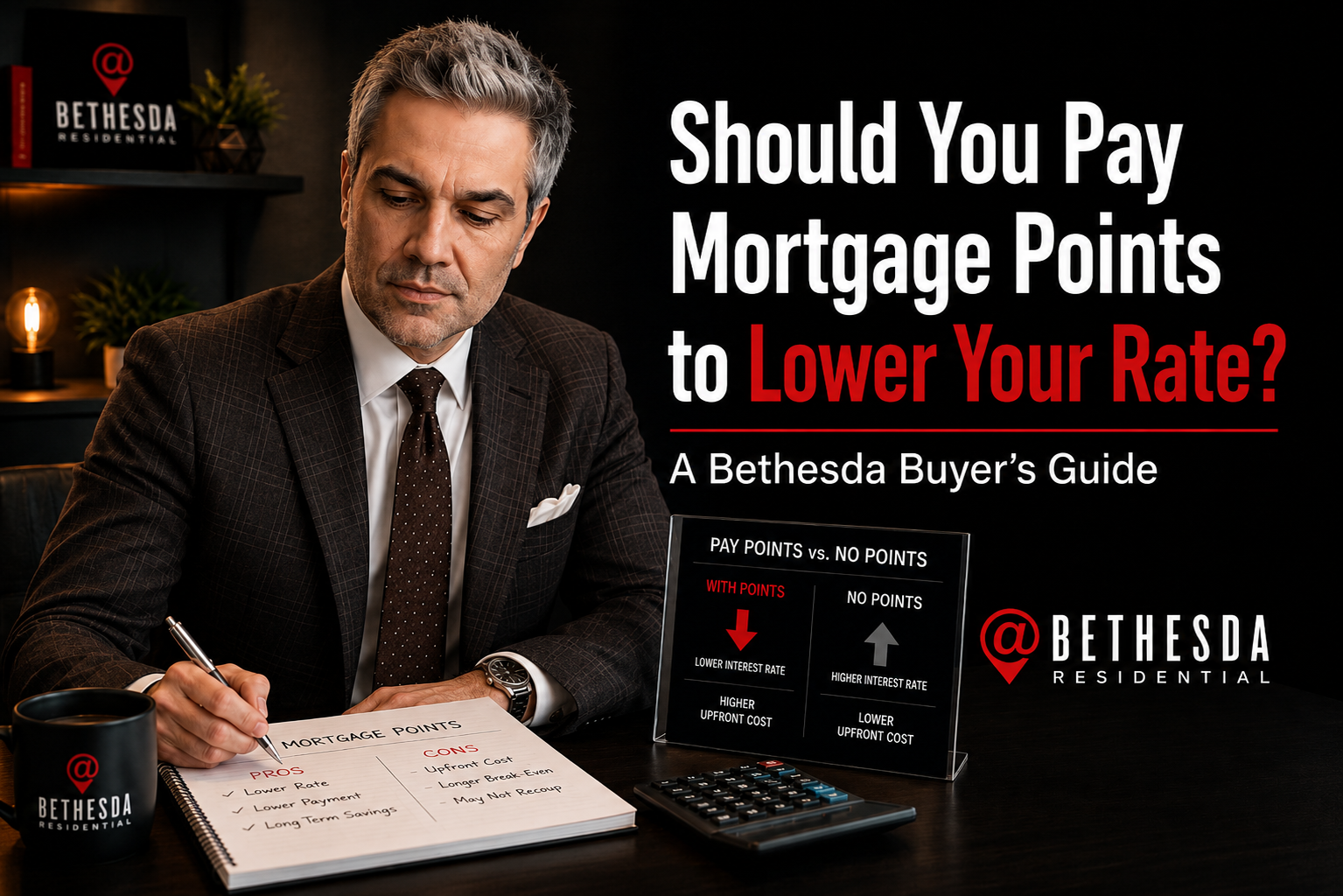

TL;DR: One mortgage discount point = 1% of your loan amount, typically buying a 0.25% rate reduction. On a $1M jumbo loan, that's $10,000 upfront for ~$165/month in savings — a break-even of about 60 months. Points make sense if you're staying at least 5–7 years and don't expect rates to drop enough to refinance within that window. In a 6.5%+ rate environment with refinance expectations on the horizon, the math is less clear than it looks.

How mortgage points work

One discount point = 1% of the loan amount, paid at closing to permanently reduce your interest rate. The rate reduction per point varies by lender and loan type, but typically runs 0.20%–0.375% per point. On a Bethesda jumbo loan at 6.7%:

- Loan amount: $1,000,000

- 1 point cost: $10,000

- Rate reduction: ~0.25% → new rate 6.45%

- Monthly savings: ~$165/month

- Break-even: $10,000 ÷ $165 = ~61 months (just over 5 years)

The refinance wildcard

Points make most sense when you plan to hold the loan for the full break-even period. But in 2026, with 30-year rates around 6.5%–6.7% and forecasts suggesting rates may ease to 6.2%–6.5% by late 2026, many buyers expect to refinance within 3–5 years. If you refinance at year 3, you paid $10,000 for 36 months × $165 = $5,940 in savings — a net loss of $4,060.

This is the core problem with paying points in a "wait to refinance" environment: you pay them upfront but may not hold the loan long enough to break even before the refinance resets your mortgage.

Temporary buydowns (1-0 and 2-1)

A temporary buydown is different from paying points. A 2-1 buydown reduces your rate by 2% in year 1 and 1% in year 2, returning to the contract rate in year 3. Often seller-funded (a common negotiating tool from builders), the cost is typically 1.8%–2.5% of the loan amount. On a $900K loan, ~$16,200–$22,500 upfront, paid by the seller as a closing cost credit.

Temporary buydowns help with initial cash flow but don't change the long-term economics. Good for buyers who expect income growth in years 1–2 or who are confident rates will drop enough to refinance before year 3.

When points make sense in Bethesda

- You're confident you're staying 7+ years

- You don't expect to refinance (rates are at or near long-term bottoms)

- You have the cash to pay points upfront without depleting reserves

- The rate reduction is at least 0.25% per point (shop multiple lenders — rate per point varies)

When to skip points

- You expect to refinance within 3–5 years (likely if rates drop)

- Cash is tight — preserving closing cash is more valuable than monthly savings

- You might move in under 7 years due to job, family, or market changes